All Markets Pay Fealty to Washington

When Once again, the world is held in thrall by the policies of Washington. Stock markets rejoiced yesterday in the climbdown of Canada delaying implementation of the digital services tax (DST) on the US tech giants opening an opportunity for renewed trade talks between Ottawa and Washington. It appears the ever-bulls in the stock market see more last-minute deals developing even though negotiations between the US and other centres of commerce such as Japan and Europe are causing comments of frustration from the US President. Bourses neared all-time highs, and it is interesting to note that the marathon debate in the US Senate regarding the ‘big, beautiful bill’ in which the US Government will accrue another $3.3 trillion in debt, worries stock market investors not a jot. Today the ‘vote-a-rama’, a succession of amendments to the bill, will be seen but the bill’s passing creeps ever nearer. It appears markets are dwelling on the tax incentives and likely liquidity injection rather than debt, civil cuts and the threat to US treasuries.

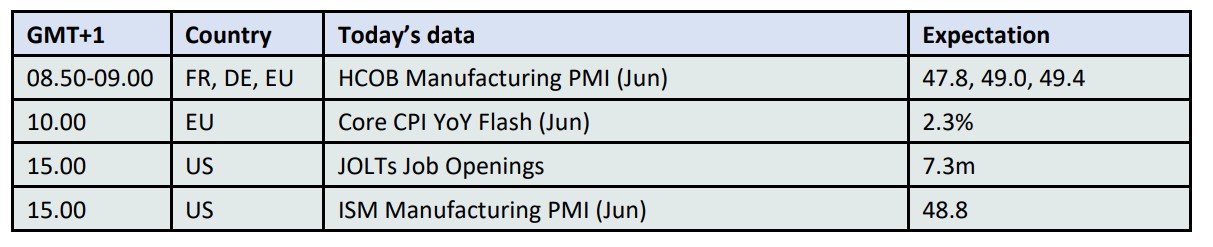

Oil prices on the other hand, once again adopt the role of echoing what might be going on in the industrial world. While manufacturing PMIs in China, Japan and South Korea improved, they hardly bore evidence of industrials going great guns. Indeed, within the comments from Asia countries, all were uniformly agreed on how the influence of tariffs were still darkening the horizon. Given the relative calm in the Middle East, relative being appropriate, the geopolitical premium for oil prices is unable to insulate them from a corrective slide. With the almost assured announcement of another 411kbpd of OPEC+ cuts this week for return in August, participants in our community are rightly staying out of harm’s way.

OPEC’s wane as refiners’ influences wax

As we approach yet another OPEC meeting this week, the world and its oil interest will be very much expecting another bout of production relaxation. There is little to suggest the cartel will not carry on hell-for-leather in its newfound quest to wrestle market share back from those that have benefitted from its misjudged attempt to manage price by supply. Having busted their own flush and with its total output influence into the world on track to fall to 30% of supply, the cartel must wait for better times for oil prices and along with the rest of us take note on how hard, or not, refiners are working to strike a price/demand balance. Supply/demand balances are all well and good, but they have not served OPEC well for some time.

It is hard to speak on consistency, we live in such inconsistent times, but in general terms prices of refined products tend to have slower price reactions than that of their feedstocks. There are of course many cases when stressful periods for individual fuels in times of troubled weather or storage and pipeline accidents create short-term anomalies but overall, it is fair to say that expressions of bullishness or bearishness is more likely initially seen in Crude prices. This is also accentuated by investment monies that require a greater liquidity base, one that cannot be skewed by the levels of the Rhine or whether a fuel is summer or winter grade. In times of flux, products are either in the middle of having heat or chemical processes applied within a refinery or are indeed in a tank somewhere largely with a destination in mind. Much of crack values are determined by the fortunes of Crude rather than specific weakness or strength in say Gasoline or Distillates.

The role then of refiners is to police all the processes involved in keeping a ‘Goldilocks’ supply of oil derivatives available for global consumption. It is not as simple as running to suit where demand for individual product might be; account must be taken for sweet/sour differentials as well as complex freight and storage charges. Clearly this is no altruistic enterprise, keeping the reins tight on what enters a processor and what comes out is a commercial practice driven by profit so ably recognised as ‘refiner margin’. Therein lies power. It matters not that a super refiner can run 500kbpd of crude, if it only makes money by running 400kbpd, guess what it will do? There is a natural instinct to believe that in the presence of continued lower Crude prices, refiners can ‘make hay’. It can also be assumed and argued that in times of supressed feedstock prices, demand for lighter products increases because the rush to efficiency and alternative vehicular power loses momentum. However, any such assumptions require this market state to exist into the longer-term, something we all have given up on predicting and crystal balls have long since disappeared in this topsy-turvy world.

Ultimately healthy Crude demand is subject to refined product use. Refiners will only crank up processing if differentials are suitably profitable. In this, comparisons can be made with OPEC+, refiners will shutter runs in times of demand drought and margin but are not in the business of creating vacuous demand by withdrawing long-term supply from the market. At present refinery runs are nowhere near capacity from the US to China and even though because of turnarounds, Distillates stocks are shrinking, whereas the summer has yet to show up for Gasoline. Product inventories are low and warn of possible problems to come. However, in these mad times, refiners have every right to live out a hand-to-mouth existence in the face of an oil fraternity worrying on being overly long inventory in a world that is not trading properly. Coupled with high interest rates, and daily threats from EV rollouts, the refining community will keep seeking the margin sweet spot. The decisions they make may all be about the here and now, but at present companies that are in the business of oil processing are the arbiters of demand and oil market health.

Overnight Pricing

01 Jul 2025