Another Week of Reality Check

It is looking increasingly likely that one day, though not in the immediate future, the Old Continent will be grateful to the omnipotent leader of the New World. No doubt, military reliance on the US over the past 80 years has proven unhealthy, has led to inertia, and President Trump, to a certain extent, justifiably, has run roughshod over former allies. His latest salvo was manifested in the relentless pursuit of ‘owning’ Greenland. This coercive move, however, was deemed to be over the line and made alarm bells ring louder in Europe than at any time since WWII. There are now tangible and explicit attempts to become independent from the US, as so forcefully put by the Canadian Prime Minister in his brilliant speech in Davos, for which he received a standing ovation. Of course, these attempts do not go unnoticed in the White House, and its tenant re-launched its threat of 100% import tariffs on the US’s northern neighbour, if the Canada-China trade deal, negotiated last week, is, in fact, implemented.

The flare-up in tension between the US and Europe, and the very real threat of re-igniting a trade war by imposing reciprocal import tariffs, sent investors searching for safety, as equities were sharply sold off mid-week, coupled with a ravenous appetite for gold, which broke above $5,000/ounce overnight. Naturally, nonetheless, there was a twist. Akin to the ‘Liberation Day’ act, the climbdown from the US ultimatum to annex Greenland one way or the other, even by the use of military force, was spectacular. The difference between last April and this January, apart from pragmatic investors expressing their disapproval beyond doubt, was Europe deciding to fight its corner instead of resorting to sycophancy, and the voices of discontent from within the Republican Party also becoming louder. There is no sugar-coating last week’s major development: it showed that firm opposition and unity are the most formidable weapons against extreme and myopic foreign-policy strategies, which could otherwise have unnecessary repercussions for economic prospects. Equities recovered from Tuesday’s slump. The MSCI All-Country Index closed 0.18% higher on the week and 2% above the lowest print.

Cheap or Dear? Bang in the Middle.

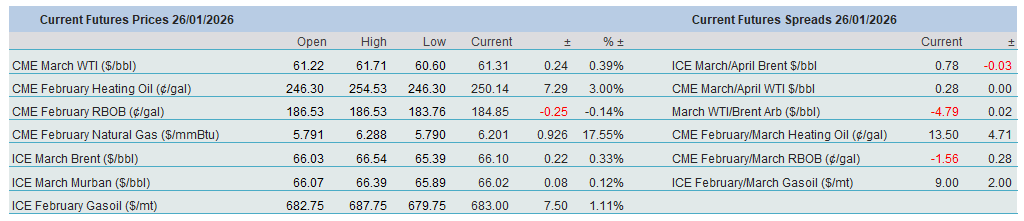

It is all very well that updated projections on the global oil balance are scrutinised every month. It is also understandable that, since they imply swelling oil inventories in 2026, price forecasts, including ours, are rather pessimistic, or at least conservative. The latest poll of analysts by Reuters, published at the beginning of January, indicates a mean Brent price of $61.27/bbl for 2026, matching the median forecast. This is $7/bbl below the 2025 average. Is this a reasonable assumption? Is it too high or too low?

A good starting point is the futures curve. Sticking with the European crude oil marker, the structure of the curve remains in backwardation for the next 12 months or so, after which it flips into contango. Does this suggest tightness in the coming months and oversupply from 2027 onwards? There appears to be no shortage of oil. This is what the monthly data and the weekly EIA reports on US commercial oil inventories imply. Global oil stocks are expected to rise every quarter this year (although estimates of absolute figures swing wider than a pendulum), while industrial stockpiles in the United States are sitting comfortably above both last year’s level and the seasonal norm. They have increased by 40 million bbls since last November.

Historical comparison is equivocal. It is curious to observe that, using the latest set of data from OPEC, projected OECD stocks, stretching from 2.871 billion bbls in 1Q to 2.966 billion bbls in 4Q 2026, are very similar to inventory levels registered between 2016–2018, when Brent fluctuated around the $60/bbl mark, close to this year’s price forecast. As frequently pointed out, OPEC is the most optimistic about the call on the group’s oil, a view aligned with that of Aramco’s CEO. Amin Nasser, during last week’s World Economic Forum, made it clear that he believes predictions of a glut are seriously exaggerated, presumably referring to the IEA’s and the EIA’s estimates.

The current price level, the futures curve, and the consensus on this year’s price forecasts corroborate his prognosis and OPEC’s outlook. The steady increase in US commercial stockpiles, which account for around 45% of OECD industrial stocks, does not. As discussed in Friday’s note, the cold winter in the northern hemisphere is seen as a seasonal pillar which, once withdrawn, could lead to a retreat of several dollars. One must not forget about Russia, Iran, or Venezuela, the collective noun for which is risk premium. Yet while distillate support will gradually evaporate as temperatures rise, risk premium, given the fragility of the state of the world, will not. In addition to swelling oil stocks, both on land and sea, another counterargument to higher prices, however trivial and peripheral it may sound, is Donald Trump’s declared target of pushing the price of oil down to $50/bbl, with the help of Venezuela.

Last week’s performance indicates that oil market participants fully acknowledge the presence of these opposing forces: OPEC’s upbeat view, distillate strength, and fears of unintended oil shortages, versus diverging supply-demand estimates insinuating substantial stock builds, the transitory support stemming from the middle of the barrel, and the upcoming US midterm elections, which will incentivise the incumbent administration to keep retail gasoline prices, and, by extension, crude oil prices, as low as possible.

Notwithstanding all the unpredictability surrounding different asset classes, including oil, and the headline-driven nature of markets, Brent managed a comparatively narrow weekly range of $3/bbl. If last week’s and this month’s performance are a harbinger of things to come this year, then we may well find that predicting Brent to average just above $60/bbl will prove to be a very accurate call. Moreover, despite, or perhaps because of, the ever-increasing number of ‘known unknowns’, the annual trading range may be much narrower than in recent years.

Overnight Pricing

26 Jan 2026