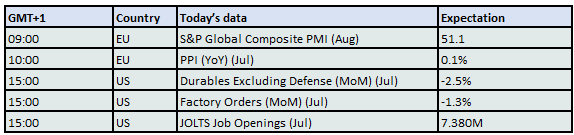

A Brief Glance Away from Oil

It is difficult to predict how long the foul stench of debt currently blowing though economic halls will last, but it is a timely reminder that AI does not solve everything. Equities in September are etched in market lore as being a troublesome month and so far, such superstitions are proving founded. In the US, doubt was born last Friday on the appeals court ruling on tariffs, the other uncertainties that have laid fallow seemed to have germinated from there and where all woe had been covered up by Nvidia and its like, the bond fundamentalists now concern themselves with the Fed’s independence, the ballooning overvaluation of US companies and a slowing American economy as depicted in the ISM Manufacturing PMI. Nervousness is pronounced in the bond markets and yields have taken a hike, which is most unwelcome in a period when a spate of new bond issues globally is about to be auctioned. Breaking down the accompanying debt concerns in Japan, France and the UK would be too word heavy, but the chill of their failing or flailing governments that are overloaded in borrowing, cuts a comparative theme. Given the power of influence from bonds and a political landscape far from steady, risk-off is set to continue. However, can even risk-off be relied on? Given a September ‘reset’ and political incertitude, it is little wonder that the greatest safe haven of all, Gold, is well and truly back in vogue.

All that glitters is not oil

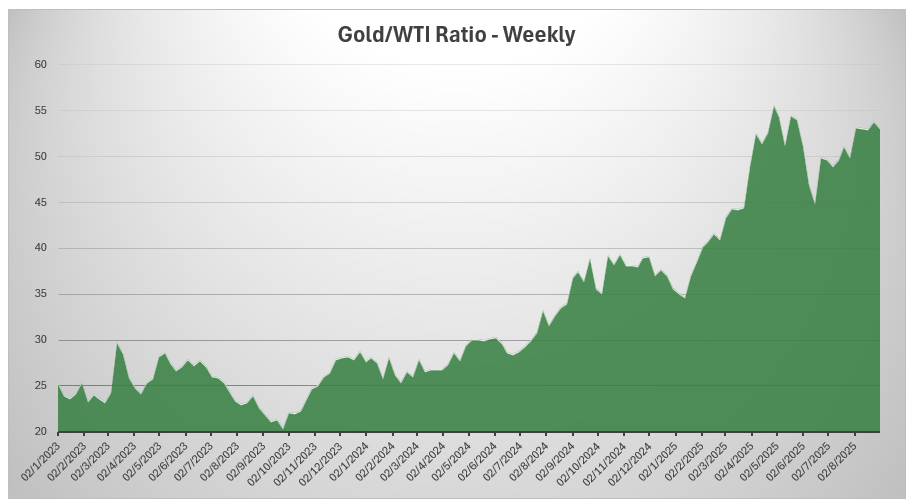

In yesterday’s report my colleague reminded us on the diverging price and investment plot being pathed by oil and equities. With this in mind it is also worth pointing out that it is not just equities that oil has an unfavourable outlook when put up in comparison. Notwithstanding a spike in the Gold price when the US placed a 39 percent tariff on Switzerland last month and the landlocked country’s association with bullion trading particularly the export of 1kg bars, Gold has once again found favour after spending a goodly time in consolidation this year post-Trump election win and the storming of $3000/ounce. Yet, the contemporary rise owes its beginnings much before the Donald entered the White House and started at the back end of 2023. Strategic length and de-dollarisation flew in the face of higher interest rates seeing in a sustained rally and a doubling of Gold’s price from $1800/ounce to $3500/ounce. Taking a look at the chart below, it clearly shows the outperformance of Gold over oil in the same period. Barrels of oil to ounces of Gold has increased from just over 20 to nearly 55, which is a steeper increase than the actual price of Gold itself.

There is also little doubt that Gold prices are very much helped by the fortunes of Silver. So long the ugly cousin in the dungeon, Silver has at last been released due to its favourable use in industrials. As the world’s reliance on critical minerals and precious metals increases Silver has found a latter-day relevance in circuit boards, connectors, switches, EVs and solar panels. Its conductivity and accepted historical uses in medicine, chemical manufacturing and production of alloys never brought enough demand to match its Copper and Gold elemental periodic table partners. However, because of the increased demand of modern technology and that Silver production is at times limited being a biproduct of Lead, Zinc, Copper, and Gold extraction, its case for being part of investors’ portfolios has increased dramatically. The sophistication and knowledge of American retail investors mean the US is still the source of much of Silver’s demand, but its strategic importance is not lost on China’s striving for independent, economic stability. Given China’s global lead in all modern forms of energy-switching Silver’s newfound interest is unlikely to wane with there being many more reasons to hold it rather than just its historical use in jewellery and photography.

Geopolitically, what is not lost on markets is the recent love-in between China, Russia and India. New Delhi is fed up being a punching bag for Washington whims and it is self-evident how China, Russia and the other members in the BRICs brigade are at pains to extricate themselves from the clutches of the US Dollar and how it is weaponised time and again by the United States. If the US is bent on changing the make up of the world’s trading pattern with the imposition of tariffs, the pushback is coming from how affected nations will continue to move away from any spheres of influence Uncle Sam controls. Uncertainty in global economics will continue to drive the prices of precious metals be they unrest, wars, recessions, weather events and the ever worry of inflation. In inflationary times, asset values decrease giving even more reason to own the very best of tangibles such as Gold and the other precious metals. Unlike oil, this confluence of demand will more than match supply, the very reason fundamental trading length is undertaken. Yes, our market will see a Distillate season, we are way behind in building the mainly winter fuel stock, and yes, oil prices are always about the end-product. However, bearing in mind the weight of crude supply that will burgeon the oil price future, does the current Gold to Oil ratio really signify oil being undervalued?

Overnight Pricing

03 Sep 2025