Fragile but Holding

Despite the announcement of a ceasefire between Israel and Iran in the early hours of yesterday, missiles and mutual accusations of violations continued to fly back and forth — much to the chagrin of President Trump, who brokered the truce. He did not shy away from publicly reprimanding both parties for the disobedience. While a number of questions regarding the deal and in fact the effectiveness of the US strike on Iran’s nuclear capabilities remains unanswered, the fact that the agreement is still in effect has been met with a massive sigh of relief. Investors rushed back into equities, although US consumer confidence has deteriorated this month, and Fed Chair Jerome Powell remained tight-lipped about when interest rates might be lowered. Meanwhile, the US 1Q current account deficit — driven by tariff-induced front-loaded imports — reached a record high.

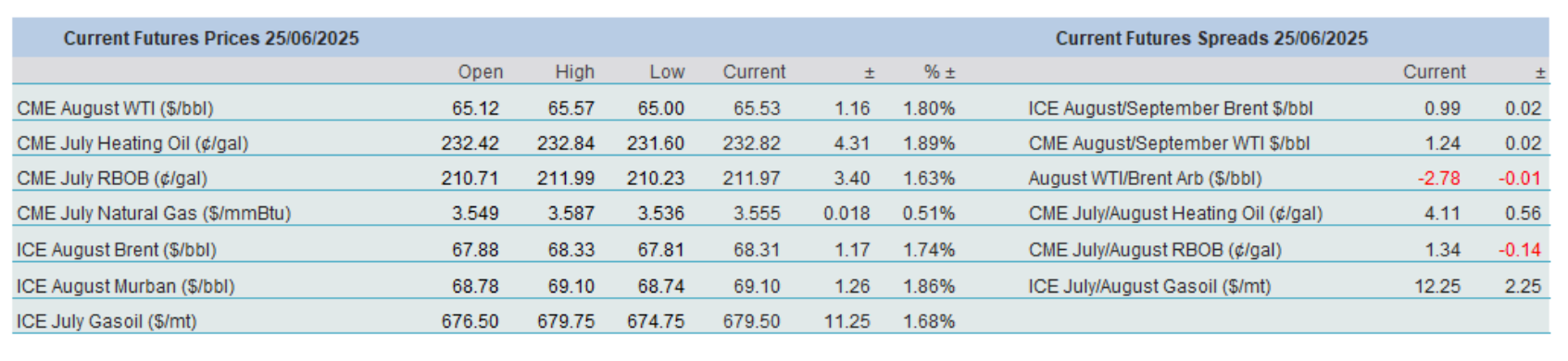

As the likelihood of a severe supply disruption in the Middle East has diminished considerably, the stampede out of oil continued yesterday, following Monday’s sharp decline. Over two days, from high to low, the European crude oil benchmark fell by $14.58/bl, or 18%. Whether optimism about a secure oil supply in the foreseeable future will be sustained remains to be seen. The good news is that the US President remains characteristically confident. In a social media post, he signalled approval for China to resume purchasing Iranian crude oil by opting not to enforce existing sanctions on teapot refiners. As long as relative calm is maintained, factors such as tariffs, trade talks, the US budget, and oil inventories will shape the investment landscape. The morning’s bounce is most probably the function of last night’s API report, which showed considerable drawdowns in crude oil and distillate inventories with gasoline stockpiles up a tad. Volatility will persist, though not to the extent seen over the past week or so.

Abundance of Supply

One of the most salient aspects of the tension in the Middle East—particularly for those involved in oil trading—has been the security of oil production, supply, and transit in the region. The broader picture shows that the combined output from Saudi Arabia, Iraq, Kuwait, Iran, Bahrain, Qatar, the UAE, and Oman amounts to nearly 23 million barrels per day (mbpd), over one-fifth of global production. The lion’s share of this oil, along with a significant volume of LNG predominantly from Qatar, passes through the strategically pivotal Strait of Hormuz. From there, European and U.S. shipments make a sharp right turn as they leave the Gulf of Oman, another right at the Gulf of Aden, and continue through the Bab al-Mandab Strait—near Yemen, home of the Houthi rebels, an Iranian proxy group. After cruising up the Red Sea, vessels must navigate the Suez Canal before it’s plain sailing to European or American destinations.

For the reasons mentioned above, political stability in the region is imperative and an absolute must to ensure a reliable supply of energy all over the world. After Israel launched its strikes against Iran on June 12 and the US joined in last weekend, oil prices rose from $68/bbl to over $81/bbl basis Brent in the space of 11 days. When a tentative truce was struck between the Middle East adversaries and when the market grew in confidence that the production boat would not be rocked, the result was a nearly unprecedented price plunge.

Assuming -but not fully trusting- that this auspicious status quo will be maintained, the latest round-up of production figures suggests that there will be no shortage of oil. Smaller disruptions will be easily replaced by the readily available spare capacity, provided that crucial arteries remain open. As referenced in Monday’s report, Energy Intelligence (EI) assesses OPEC+ adjusted spare capacity at 6.75 mbpd, and when constrained capacity is added, this figure goes up to 7.3 mbpd. The EIA estimates that OPEC’s spare capacity will sit comfortably above 4 mbpd throughout the last quarter of 2026.

This reassuring backdrop is coupled with more than comfortable supply estimates. Circling back to EI, its latest projection shows global output, which includes crude oil and other liquid supply, at 104.165 mbpd in May, a monthly increase of 736,000 bpd and the highest on record. It is well worth pointing out that this record was achieved with a substantial supply cushion to fall back on. Crude oil supply stood at 77.736 mbpd, with other liquids at 26.429 mbpd. The above-mentioned 736,000 bpd growth was concentrated in countries that are not party to the OPEC+ agreement (510,000 bpd), and the extended producer group registered a monthly expansion of 149,000 bpd, with OPEC itself up 208,000 bpd. (The difference of 76,000 bpd between the total and the sum of the parts is attributed to refinery gains.)

The fact that 70% of the monthly growth came from non-OPEC+ nations is a clear concern for the producer group. While OPEC+ was voluntarily giving up market share to tighten the oil balance, non-member countries were quick to fill the gap. In fact, according to OPEC's own calculations, production growth outside the group has been striking. In 2022, total non-DoC (the OPEC terminology for OPEC+) production was 49.4 mbpd, rising to 53.2 mbpd two years later. For 2025, production is forecasted at 54 mbpd, with an expected growth rate of 700,000 bpd over 2025–2026.

It was, therefore, only a matter of time before the group abandoned its output restraint policy and began releasing more barrels back into the market. Past attempts at market management have proved largely ineffective, and with OPEC holding a relatively optimistic view on demand, the unwinding of cuts has been accelerated. If all goes according to plan, 2.2 mbpd of OPEC+ oil will be added to global supply by September.

Although projections vary significantly on global oil demand—and risk premiums could spike abruptly if geopolitical tensions escalate in the Near or Middle East—in a tension-free environment, oil supply will not be the driver of a structural bull market. And considering the current economic outlook, neither will oil demand.

Overnight Pricing

25 Jun 2025