Markets In the Mood for a Deal

An incredible testament to market and investor psyche has played out post the US/UK tariff deal. After months of a perceived trade war due to the tariff policies of Donald Trump’s White House, the first piece of ‘good’ news, as in a deal, seems to give visions of a vista where further global negotiations will be simple and a more harmonised trade environment and mutually pleasing outcome is achieved. The market reaction sadly ignores that the UK might just be a test case for the US as it hones its skills when faced with trickier opponents across the negotiating divide. As it is, the UK has agreed to cut tariffs on US goods from 5.1 to 1.8 per cent, whereas the US will triple UK tariffs from 3.4 per cent. Therefore, the baseline 10%, apart from steel and aluminium, that was originally threatened is now the standard and while principles are always abandoned at the doorstep of pragmatism, UK to US exports at a tenth higher will need to be paid for somehow, by someone.

Odd then that investors have chosen such a deal as a possible pathfinder, it is the UK after all, it always does what the US wants. If the market deems success at cracking a deal at 10 percent compared with the threatened 25 percent, it must expect some sort of miraculous write down of the 145 percent tariffs currently bandied around by The Donald when talking on China’s trade surplus with the US. It is this hope that stands for a near 3% rally in Brent futures prices after a day where many other risk assets were encouraged higher on the same news. Still, the oil market upswing was aided by reports on a reaction by Chinese refineries being seen due to US sanctions surrounding Iranian oil. According to Reuters, using Vortexa data, China has been seeking crude sources elsewhere and although imports were lower from the previous month, year-on-year imports has increased from 10.88mbpd to 11.69mbpd in April. With a Reuters survey showing OPEC oil output being reduced in April due to issues in Libya and the bite of sanctions on Venezuela, production was down 30kbpd despite the announcement of the returning voluntary cuts. All just enough to add an extra glimmer to the hope being displayed for the Sino/US talks tomorrow.

War is hell, uncertainty for markets is not much better

It is strange to see the airwaves and telecasts filled with WWII veterans and civilian survivors reminding the world that “war is hell” as yesterday saw the remembrance of 80-years since VE Day. When considering that state of the current conflicts around the globe it is does beg whether any lessons have been learned at all. Religious and race intolerance, expansionism and mineral envy are not just the remit of the past, they are alive and will in contemporary times as witnessed in Gaza and its Middle East neighbours, in the Ukraine and Kashmir. Listing all the conflicts and atrocities that occur on a daily basis would lead to a bout of depression, but nonetheless at historical times of reflection it is worth noting how far humanity has come and whether we stack up to the warnings of our elders and betters.

While we may not be under a military world war, we are certainly under a trade one. It would take a Socratic debate as to whether losing livelihoods is as important as losing lives, but the anxiety felt in the world is palpable. However, where there was certainty and conviction from the ‘greatest generation’ as to the path to peace, contemporary considerations are governed by flighty egoist world leader’s whims and their apogee, Donald Trump. Markets await the scathing response that will assuredly be meted out toward Jerome Powell, the Chair of the Federal Reserve, as the US Central Bank kept its interest rates unchanged on Wednesday, but Jay was stoically unapologetic in his post-decision press conference. Some quarters have been asking for a tariff protecting interest rate cut, the irony all but screams, but the Fed Chair batted the idea away, “It’s not a situation where we can be pre-emptive, because we actually don’t know what the right responses to the data will be until we see more data.” He is indeed right, the metrics have been mixed of late and include how April’s Non-Farm Payrolls showed healthy employment, but GDP was all weakness and missed expectation by some mark. The FOMC was unanimous in its decision to hold rates but belies anxiety. This is mirrored by the Bank of Japan that toils under pressure to increase interest rates but runs scared of a downturn, and the European Central Bank that must reduce them as the only means to revive a flat-lining economy even at the risk of inspiring higher inflation. If the world’s central banks, analysts and indeed oil journals such as the EIA STEO congregate around a word it is ‘uncertainty’.

This spills into the weekend and despite a much-lauded deal with the UK, which frankly has been an understandably sycophantic affair, it is hardly likely a quick fix deal between the United States and China will occur during tariff talks in Geneva. China has all but called the US a bully and declared it will be immune to Washington’s coercion. In turn, and as the US Treasury Secretary Scott Bessent heads to Switzerland, Donald Trump said late on Wednesday he was disinclined to reduce tariffs for the sake of negotiation and lately has even gone as far enough to say, "we're losing nothing" by declining trade with Beijing. Therefore, a meaningful end to trade hostilities appears to be a longshot, but in this world of fluid expectancy and delivery, a rabbit of hope might just be pulled from the hat. Either way, markets will, in defensive football parlance, start ‘parking the bus’ into the weekend because deal or no deal, reaction is likely to be sharp Monday morning. ‘Uncertainty’ reigns over all it sees and those that come under its gaze are wise to stay vigilant.

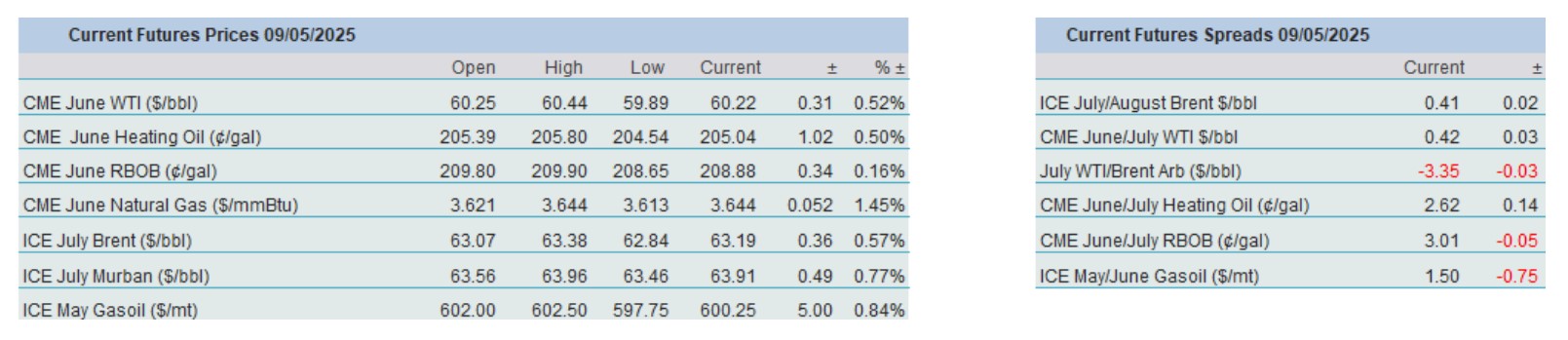

Overnight Pricing

09 May 2025