Supply Under Scrutiny

After the calamitous US tariff announcement on April 2, all hell broke loose in financial markets. The MSCI All-Country Equity Index dropped 14% in less than a week. US stock indices matched the global performance. Frighteningly, the dollar was sold off and so were US bonds, deemed the safest of investment destinations. The US 10-year bond yield rallied to 4.6% whilst an unprecedented stampede into gold pushed its price briefly above $3,500/ounce. As the dust settled on the announcement, nerves have been calmed, and the recovery began. By last Friday all the lost territory in equities was re-captured. Despite the dollar being sold off against Asian currencies, its index sits comfortably above the April trough, bond yields, although still nervous, have stabilized and gold has also been on the retreat from its record high in the first half of April. The reasons for the reversal are twofold. Firstly, economic data was somewhat sanguine. The US economy shrank in 1Q, the contraction was believed to be the result of stockpiling ahead of tariff announcements. Consumer spending, inflation and job data have, so far, proven resilient (but will likely deteriorate in the coming months). US nonfarm payrolls in April rose faster than projected. The service sector growth also beat expectations, as reported yesterday by the ISM. Secondly, because of the initial bleak market reaction, the US administration dialled back on the rhetoric as well as on the implementation of import taxes. Corporate and market pressure forced the Trump apparatus to pause the steepest duties for 90 days, exempt some Canadian and Mexican goods, turn lenient on the car industry, and promise help to the agricultural sector.

The recovery observed in stocks, the dollar and bonds, nonetheless, has failed to permeate the oil market. Whilst equities have scaled the April 2 peaks both WTI and Brent put their April 9 bottoms under intense pressure yesterday. Brighter economic prospects, or at least the backpedalling on and the pausing of unnecessarily punitive measures have brightened the mood and as such supported oil demand to a certain extent, but at the same time more than ominous signs are emerging from the supply side, chiefly originating from the OPEC+ heavyweight, Saudi Arabia.

The group has been doing whatever it could to support the oil market. It included painting an upbeat picture of oil consumption and taking, in total, around 5 mbpd of oil off the market, including voluntary output constraints. The natural consequence of this effort was a reduction in market share. Based on EIA data, the OPEC+ alliance collectively produced 46% of the world’s total at the beginning of 2022. This market share has declined to 41% in March. The interim period saw oil prices spiking to $140/bbl in March 2022 because of Russia’s invasion of Ukraine. Still, the oil market has struggled to break convincingly above the pre-war level of $80-$90/bbl as non-OPEC+ producers happily filled the supply void left by the group.

Given that many member countries, most notably Saudi Arabia, need $90+ price to balance their budget there has been a progressive erosion of enthusiasm and trust about the effectiveness of the strategy. It has most probably not been lost on policymakers within OPEC and the Kingdom that whilst 3 years ago Saudi Arabia and the US produced broadly the same amount of oil, today the latter pumps close to 4 mbpd more than the OPEC heavyweight – an undisputable sign of the transfer of oil wealth from OPEC+ to other producers. Add to that the growing frustration from within the group about the non-compliance of several member states, such as Kazakhstan and Iraq and one could only wonder when the first signs of discontent would emerge.

Well, the moment of truth arrived at the beginning of last month when the plan of eight OPEC+ members to unwind voluntary reductions at the pace of 135,000 bpd was accelerated to 411,000 bpd for May due to a constructive fundamental backdrop, according to the official narrative. Last weekend, it was announced that the same increase would take place in June and this time it came with an explicit warning: unless the disobedient members fall in line and show restraint, the unwinding of the 2.2 mbpd of cuts that was planned to be implemented in 135,000 bpd monthly increments lasting 16 months will be over by November.

The combination of ineffective market management, shrinking market share and the weakening of internal cohesion sends a negative message to the market. If this abrupt shift in the modus operandi is not reversed swiftly then the 2H global oil balance will have to be re-evaluated shortly. To quantify it, under the latest assumed scenario 2.2 mbpd will be added back to the market in lieu of the 8*135,000 bpd = 1.08 mbpd planned originally. Further weakness is being anticipated as manifested in yesterday’s $1/bbl drop in the prices of the two major crude oil benchmarks. However, the potential output increase must be viewed in the entirety of the oil balance. The initial impact is bountiful oil supply and possibly depressed prices followed by slowing output growth in non-OPEC+ countries, particularly in the US shale sector, increased chances of maximum pressure on Iran and finally oil demand support, especially if US trade policies will not precipitate further economic damage and credibility and trust in the US Administration, which are currently suffering from a severe deficit, are gradually re-gained. Because of the huge amount of uncertainty surrounding the macroeconomy, it is challenging to predict the extent of any oil price fall. This morning yesterday’s losses are being re-couped. Whilst it is most plausibly not the beginning of a protracted recovery, timewise the pain caused by the OPEC policy reversal might prove brief.

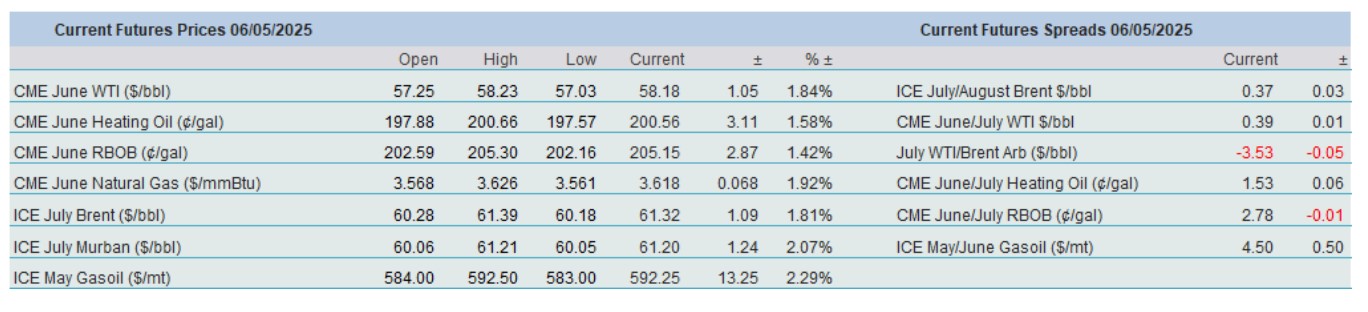

Overnight Pricing

06 May 2025