Tariffs Aside, Might Rich Stock Markets Sponsor Oil?

Even after six months of tolerating the modern phenomena of ‘Trump tariff trending’, it is a shame markets cannot develop a pattern of consistency matching the constant that is the President’s edicts. Notwithstanding the intestinal fortitude of those interested in US bourses to add to portfolios, markets continue to run an almost hourly endurance of ‘what next’ from the White House and whether it will be the one that sends all the buyers packing.

The pace and ante of the US tariff assault on trading partners has been upped this week, and whether it is another negotiating bluff will only be realised come the next expiry date by when nations must act, which is now August 1st. Being a resident of the Americas proves to offer no preferential treatment. Following the crippling intention of a 50% tariff on Brazil, along with political meddling aimed at undermining a charge of sedition against the previous right-wing President Jair Bolsonaro, overnight the US President once again brought Canada back into his list of antipathies. Beggar thy neighbour indeed, as late last night a letter to Prime Minister Mark Carney was released on ‘Truth Social’ on how the current rate of 25% levy would be increased to 35%. The tariff is not exactly clear cut, there are exemptions for goods under the USMCA and for energy, but the overall effect is galling for all types of trading markets and is the singular reason oil prices are currently facing a setback.

Oddly enough, it is the TACO (Trump always chickens out) echo which adds to all post-tariff announcement dips being deemed as opportunities rather than warning and the self-propelled ensuing buying that keeps US bourses tickling all-time highs. If this type of one-dimensional trading is accepted as behaviour, then there is little wonder that the darling of all stocks, Nvidia, is being ‘scooped’. The AI driven rally in the tech behemoth has astonishing statistics. Its share value is up over 15% since the beginning of June, 22% higher than the start of the year and is fifteen times above the price seen in the pandemic. Given such interest and that within eighteen months its market value has doubled from $2 to $4 trillion, it is not just fear of missing out driving stock markets, it is growing profits that are ploughed back into shares. There resides massive danger to the fate of the investment world being tied up to this proverbial deck of cards, but it is hard to pick another market where investors, be they individual to institutional, have never been fatally hurt for many years.

Indeed, in the UBS Global Wealth Report of 2025, it noted the world’s population in general increased wealth and reported the Americas expanded their share of global wealth in USD from 37.3% in 2023 to 39.3% in 2024, at the expense of APAC and EMEA, whose share shrank by one percentage point each, respectively falling to 35.9% and 24.8%. The report held that much of the wealth creation in the United States came from a financial basis and was inspired by the increased value of US investments. As an interesting aside, over half of global wealth finds homes in the US and China, the ultimate source of the global trade war.

The US exceptionalism is in fact US stock market exceptionalism. Given the expertise surrounding bond trading, yields, debt and all the other dominions of the Wall Street warriors, to where should everyday Americans and global investment tourists proceed with their capital? Currencies are a destination to go to when fear sets in, and who would touch the US Dollar undermined by debt and trading policies from the current US Administration? Commodities in general are at the mercy of incoherent trade climes and worldwide pulldowns in GDP. None can be more of an example on how domestic prices of copper are flying in the US compared with those left behind in the other centres of metal trading after President Trump wanders into a 50% tariff muse on the almost-precious metal. There of course is, and always will be, Gold, the ultimate long-only asset. But stock market pickers will tell you that trading tangibles does not offer a dividend as a bonus; any positive outcome can only be realised when the asset is sold. The ancient home of investment is trading at such high, emotive levels that it is becoming hard to justify a fresh entry. Such argument has beset Gold forever, and is always wrong, well, eventually. But Gold is in a period of stutter, it has not moved much away from $3300/ounce for over three months based on M1 Comex futures. In fact, it showed signs of being overbought in April and since then the daily momentum has fallen to now register in negative territory. Probably a time to buy then, but not for stock pickers who have almost instant gratification with the likes of Nvidia.

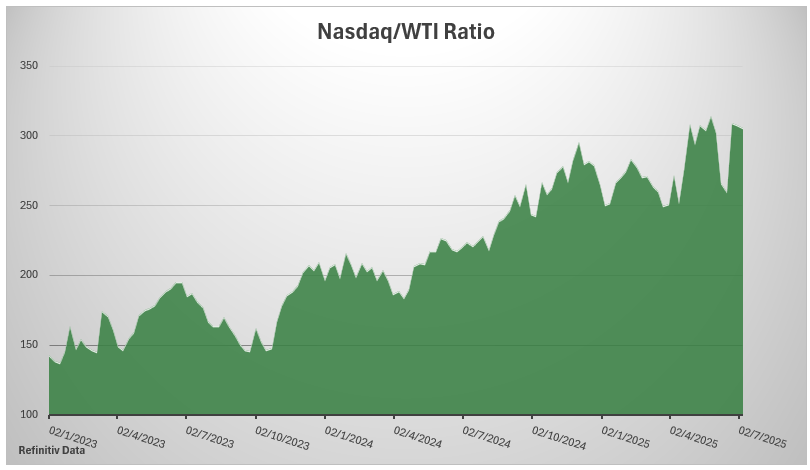

Is this at all relevant to oil prices? Well, probably not at present. But the stock market to crude oil ratio is increasing to such a large differential it must be intriguing to those made rich on stock market length. It is probably likely to increase bearing in mind the passing of the tax and spend bill in the United States where any loose monies always find themselves poured into stocks and shares. Despite a market-wide expectation of an oil glut at the back end of this year, the current spate of drivers is lacking anything that might send prices back to the lows seen in April and May. Civilians be they in the air on the road are showing a healthy willingness to travel and the issues of distillate and medium/heavy crudes we have debated on at length. What is surprising is the lack of downward pressure seen after OPEC+ bring back shuttered barrels. Argue all one may that the increase will mainly come from Saudi, and that some producers will initially lack the ability to bring such increases back, an extra half-million barrels per day as of next month, is still a lot of feedstocks. Imagine then, if one would, an end of year where the current fundamental tightness has not abated, the Middle East premium has not let go and global investors, looking for somewhere to be long become more interested in our market. It is a decent muse.

Overnight Pricing

11 Jul 2025