There is No Shortage of Supply

There are oil-related sanctions imposed by the US on numerous countries, and potentially lifting them would reassure those concerned about the tight oil balance and depleting global inventories. Yet, the US appears content with its punitive measures against perceived or actual adversaries such as Iran and India, and there is a reason for this. By the end of this month, eight members of the OPEC+ producer group will have completed the unwinding of 2.2 mbpd of output constraints. The weekend’s talks on how to proceed were therefore expected to be a muted affair and little more than a formality, but the reality might turn out strikingly different.

As Reuters reported, insiders believe the producer alliance is considering reinstating the next batch of production cuts, amounting to 1.65 mbpd, at their upcoming meeting, sending a strong signal that regaining their fair share of the market takes priority over price support at a time when global appetite for oil is not deemed ravenous. Investors in the black stuff wasted no time reacting, sending crude oil $1.5/bbl lower. Heating oil held up reasonably well, with a daily loss of less than 60 cents/bbl equivalent. The overnight API stats, which showed an unexpected increase in crude oil and distillate inventories but a larger-than-anticipated plunge in gasoline stocks, failed to brighten the suddenly souring mood.

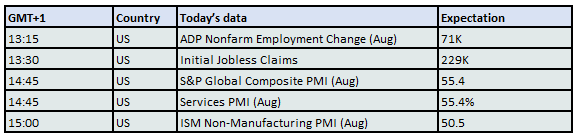

The scaremongers who predicted financial Armageddon after the recent bond sell-off have been caught flat-footed. Undeniably, ballooning fiscal deficits will cause anxiety in the near term; nonetheless, bond markets stabilised and equities soared back. Investors have grown more confident that lowering US borrowing costs is imminent after weaker-than-expected job openings, coupled with tacit reassurance from Fed officials about an impending cut. All told, tomorrow’s nonfarm payroll report is eagerly awaited and will shape expectations for the Fed’s next course of action.

Noble Lies

Studying history is not about the past. It is about meticulously analysing the changes in the past triggered by what can be categorised as historic events and attempting to envisage the future based on the shifts observed. The contemporary, and often controversial and worrisome, political and economic environment did not begin to emerge on April 2 or January 20 or even in November 2016. The start of the truly seismic shift in wielding global power is on conspicuous display in the IMF’s treasure trove, its historical data set.

Global, regional, and country-level economic data go back to 1980, when China had 2% of the global economic output, with the US claiming 22%. (The comparison throughout is based on purchasing power parity.) When China joined the World Trade Organisation in 2000, it had 6% of the whole pie, with the US at just under 21%. On the dawn of the Great Recession, China was responsible for 10% of the global output, whilst the US’s share had declined to 18%. Fast forward another 18 years, and you will find that the world's second-largest economy overtook the largest one; the current score is 20% versus 15%—a truly remarkable achievement in just 25 years.

Broadening the horizon confirms the trend described above. Advanced economies ruled the world, including emerging countries, 45 years ago, with a share of 65% of the global economic output. This year, developing nations will claim 61% of the value of total goods and services, a share which the IMF predicts will rise to 63% by 2030.

There is no need to throw additional numbers around; the tendency is crystal clear. And those who have the economic might also have the political supremacy, and they pose a direct or indirect threat to the rest. The changes observed in the past 20-25 years explain why the unipolar world order, observed from 1990, gradually turned into a bi- or even multipolar one. As a result, both sides keep telling, citing Plato, noble lies in their effort to assure their domestic audiences of the ruling elite’s best intentions to serve and protect the nation in every aspect and at any cost.

These noble lies, however, carry elements of truth, pro and con. Who could blame China for complaining about its disproportionately suppressed influence in multinational organisations, such as the above-mentioned WTO? Or the US for accusing its adversary of distorting the smooth functioning of the global market by subsidising its economy and exports, leading to dumping Chinese goods all over the world, much to the detriment of its competitors.

The developing acrimony has been discernible for years and maybe even decades. This note started by saying that studying past changes can provide clues about the future. The Trump presidency perfectly fits this narrative. President Trump’s foreign, economic, and trade policies are not the cause, but the consequence, of the shifts seen in the last 25 years. The voice might be louder, but the underlying intention remains the same: to claim political and economic hegemony. Just think of the Biden Administration also imposing tariffs on imports from China.

This week’s talks between India, Russia, and China (and 17 other nations) on the sidelines of an almost unprecedented, and frankly frightening, military parade celebrating the 80th anniversary of Japan’s defeat in WWII left no doubt about the goals of the opposing side. During this week’s Shanghai Cooperation Organisation meeting in the Chinese city of Tianjin, the host’s president underlined the danger the Global South faces, precipitated by the ’turbulence and change’ initiated by its adversaries. In the face of this danger, there is an explicit need for a ‘global governance initiative’ or ‘sovereign equality’.

When one looks up these expressions in the imaginary dictionary of political speeches, their real meaning becomes obvious: the acrimony between China and the US, or between the Global South and the Western Alliance (or whatever is left of it), will be an enduring one.

Globalisation, which lifted hundreds of millions of people out of poverty, created markets, and brought prosperity for the benefit of all who participated in it, has ceased to exist, at least for now. Economists and historians will study for decades to come whether the de-globalisation process was hastened by the scorched-earth foreign and economic policies of Trump 2.0. The objective reality, however, is that barriers are being erected all over the world, and they do nothing to brighten political, security, or economic prospects in the foreseeable future. Not only will the battle between the Wild East and the Wild West continue, but it will also plausibly intensify.

Overnight Pricing

04 Sep 2025